17 Feb Developments Reduce Spanish Inheritance and Gift Tax for Non-residents

INTRODUCTION

A unique aspect of Spanish Inheritance and Gift Tax (I.H.T.) law is that it is imposed under national law and regional law. Historically, regional rules for computing I.H.T. applied to taxpayers that are resident in the region, while non-residents applied national rules, which are not as attractive. This diverse treatment has been the subject of debate, and recent changes to I.H.T. law have improved the outlook for non- residents.

Each of Spain’s 17 autonomous regions has introduced its own set of I.H.T. rules, and the tax benefits vary widely. Each autonomous region retains the power to regulate the calculation of the taxable base, the assessment of pre-existing wealth, the computation of multiplication coefficients, the allowance of deductions, and the scope of allowances that reduce the tax due. In some cases, little benefit is provided. In others, such as Madrid, the regional benefits almost eliminate the burden of I.H.T. for taxpayers residing in that region.

While the benefits vary, the general effective rate of I.H.T. for non- residents was significantly greater than for residents under historical rules. I.H.T. was also greater for inheritances and gifts of real property located abroad than property located in Spain. This approach was deemed to be discriminatory according to a series of decisions at the European level and the national level.

In 2011, the European Commission sued Spain for breaching obligations imposed by Article 63 of the Treaty on the Functioning of the European Union (T.F.U.E.) and Article 40 of the Agreement on the European Economic Area (the E.E.A. Agreement), which mandate the free movement of capital. Subsequently, the European Court of Justice (E.C.J.) held that Spanish I.H.T. violated the right of free movement of capital in a ruling issued on 3 September 2014, Case 127/12. In response, the Spanish government amended the I.H.T. legislation in 2015.

On its face, the 2015 amendment affects only E.U. residents and residents of the E.E.A. Initially, it was not applicable to persons who are resident outside the E.U. However, in an appeal brought by a resident of Canada, the Spanish Supreme Court ruled in 2018 that the exclusion of regional I.H.T. allowances for residents of countries outside the E.U. or the E.E.A. was contrary to the E.U. concept of freedom of capital. This article will address events that struck down the Spanish system and provided equal treatment for persons resident in the E.U. and elsewhere. It also suggests a path forward for persons to reclaim excessive I.H.T. and provides some comfort for nonresidents owning a vacation home in Spain.

PRECEDENT IN E.C.J. CASE LAW

The path to non-discrimination began with three cases in the E.C.J., Jäger, Mattner, and Welte. Jäger (E.C.J. 17/01/2008 – C 256/06) involved the computation of German inheritance tax when the estate consisted of assets situated in Germany and agricultural land and forestry situated in France. German inheritance tax rules provided for a tax-free amount and the application of favourable valuation rules when calculating German inheritance tax payable by an estate when the assets were located in Germany. In the case, the agricultural land and forestry were situated outside Germany. Consequently, they did not qualify for a tax-free amount and were assessed at a higher value for German inheritance tax purposes. The E.C.J. characterized the German inheritance tax as a tax on the transfer of capital, which is covered by Article 56 of the Treaty Establishing the European Community (E.C.). The E.C.J. ruled that the German rules were discriminatory. No valid reason existed to justify disparities in valuing and taxing assets based on their location inside within Germany or another Member State of the E.U.

This article will address events that struck down the Spanish system and provided equal treatment for persons resident in the E.U. and elsewhere. It also suggests a path forward for persons to reclaim excessive I.H.T. and provides some comfort for non- residents owning a vacation home in Spain.

In reaching its decision, the E.C.J. dismissed the argument of the German government that a valid societal reason existed for the advantage provided by German law in connection with the transfer of assets located in Germany. Germany argued that the inheritance tax reduction compensated the owner for specific costs involved in maintaining agricultural and forestry activities within Germany. It also argued that the reduction assisted in preventing a forced sale by the heir in order to fund the tax payment. The E.C.J. was unconvinced by the asserted societal arguments. It concluded that the German government failed to demonstrate a valid distinction existed between an heir holding property in Germany and an heir holding property in another Member State. In both circumstances, the societal value of agricultural and forestry land existed and the economic burden of paying I.H.T. were likely the same.

As a result of Jäger, Germany revised its I.H.T. in 2008. From that point, the same tax-free allowances and valuation methods have applied to assets located in Germany or another Member State.

Mattner (E.C.J. 22/04/2010 C-510/08) also involved German rules, this time involving the calculation of gift tax. Ms. Mattner was a German citizen but a tax resident of the Netherlands. She made a gift to her daughter, who was also a tax resident of the Netherlands. The gift involved land and a private residence located in Düsseldorf. In computing the tax, the German tax authorities limited the applicable tax-free amount to €2,000, the amount allowed to a non-resident rather than the €205,000 allowance available to donors that were resident in Germany at the time.

The Tax Court in Düsseldorf sought guidance on whether the provision violated European law. In response, the E.C.J. ruled that the I.H.T. provision allowing a greater personal allowance for residents has the effect of restricting the movement of capital by reducing the value of a gift of the German property. Moreover, the restriction could not be justified by a coherent national policy. Consequently, it was in breach of E.U. law.

Welte (E.C.J. 17-10-2013 C-181/12) is another watershed case. It held that discriminatory legislation directed towards non-residents violates the freedom of movement of capital even when the taxpayer is a resident of a country that is not an E.U. Member State.

In Welte, the decedent was a Swiss national and resident. He owned property in Germany and bank accounts in Germany and Switzerland. His wife was born in Germany. She became a Swiss national and resident by reason of the marriage. She was the sole heir of the decedent’s estate. German situs real property comprised 62% of the total value of the estate. The limited deduction of €2,000 was allowed against the value of the German assets, while the non-German situs assets of the estate were not taxed. If either the decedent or the surviving spouse had been a German resident, or a resident of an E.U. Member State, the allowance would have been increased to €500,000 under German domestic law applicable to residents at the time.

The surviving spouse called this treatment into question, filing a complaint to the German Finance Court, which submitted the matter to the E.C.J. The question posed was whether unequal treatment of residents and non-residents as to matters of inheritance tax is incompatible with the free movement of capital guaranteed by the E.C.

The E.C.J. held that there is no objective difference between residents and non-residents justifying unequal tax treatment since the amount of tax on gifts is calculated on the basis of the value of immovable property and the family relationship between the donor and the recipient:

Articles 56 EC and 58 EC must be interpreted as precluding legislation of a Member State relating to the calculation of inheritance tax which provides that, in the event of inheritance of immovable property in that State, in a case where, as in the main proceedings, the deceased and the heir had a permanent residence in a third country, such as the Swiss Confederation, at the time of the death, the tax-free allowance is less than the allowance which would have been applied if at least one of them had been resident in that Member State at that time. [Emphasis added.]

SPANISH DEVELOPMENTS

In response to the E.C.J. decisions in the foregoing cases, the Spanish government continued to defend the right of its autonomous regions to apply lower effective rates of I.H.T. to residents. The result was a series of defeats in the E.C.J. and the Spanish Supreme Court. E.C.J. decision of 3 September 2014 The first defeat for the Spanish government came in a case brought by the European Commission (E.C.J. 03-09-2014 C-127/12). The European Commission claimed that the differences in the tax treatment of gifts and estates for Spanish residents and nonresidents violated Articles 21 and 63 T.F.E.U. and Articles 28 and 40 of the E.E.A. Agreement. It claimed also that differences in I.H.T. for gifts involving real property situated in Spain and comparable real property located outside Spain violated the same provisions.

In the proceedings, Spain took the position that the European Commission’s argument was technically deficient because of procedural errors and was overly broad in its approach because it failed to look at each autonomous region separately. It also argued that no national measure was involved, since regional benefits were at issue, and that, as a result, Spain did not violate any of the applicable freedoms.

The E.C.J. dismissed the procedural challenges and then ruled against Spain as to the legal matters. I.H.T. constitutes a tax on the transfer to one or more persons of the property left by a decedent person. Consequently, it is subject to the provisions of European law regarding free movement of capital. Identical treatment must be afforded to residents and non-residents, except where the constituent elements of the law are confined to items that exist within a single Member State.

Citing Jäger and Mattner, the court explained that restrictions on the movement of capital include national measures which have the effect of reducing the value of an inheritance or gift of a person who is not a resident of a State where the asset is located. Thus, a regulation of a Member State constitutes a restriction on the free movement of capital when the application of an allowance to the tax base is conditioned on residence within that Member State. The provisions of the Spanish I.H.T. rules are a restriction on the movement of capital because they explicitly provide for the possibility that autonomous regions can introduce tax abatements for residents of, or property located in, the autonomous region. From this, it follows that a person who does not reside in Spain or who owns property outside Spain faces impediments to free movement of capital because the value of property will be impaired by the increased cost of the I.H.T.

Revised Spanish I.H.T. rules

As a result of the E.C.J. decision of 3 September 2014, Spanish I.H.T. legislation was revised in 2015 to conform with the ruling. Choices were given to residents of the E.U. and E.E.A. to allow access to either the national law or the rules in a relevant autonomous region. These may be summarized as follows:

- Regarding inheritances:

If the decedent was a resident of the E.U. or the E.E.A. at the conclusion of life, heirs are given access to the rules of the autonomous region where the value of all Spanish situs assets was greatest on the date of death.

If the decedent was a resident of an autonomous region in Spain, non-resident taxpayers residing in the E.U. or the E.E.A. are given access to the rules of that autonomous region.

- Regarding gifts of real property:

Gifts made by a resident of an E.U. jurisdiction other than Spain to a resident of an autonomous region in Spain are given access to the I.H.T. rules in that region.

Gifts of properties located in an E.U. or an E.E.A. country made to a resident of an autonomous region in Spain are given access to the I.H.T. rules in that region.

- Regarding gifts of movable property:

The applicable I.H.T. rules are those of the autonomous region in which the movable property was most present for the greatest number of days during the previous 5-yearperiod.

- Regarding the proceeds of life insurance contracts:

An E.U. resident may apply the I.H.T. rules in the autonomous regions regulations where the insurance company has its domicile or the region where the contract was signed.

As the foregoing indicates, the Spanish parliament applied the E.C.J. ruling literally. The court applied a European law regarding the freedom of movement of capital, a fundamental freedom enjoyed by residents of the E.U., and addressed the effect of discriminatory treatment on residents of Member States other than Spain and property located in other Member States. Hence, the Spanish law was redrafted to extended local treatment to I.H.T. taxpayers that were residents of the E.U. or E.E.A. The revisions did not apply the same treatment to persons resident in other countries or to property located in other countries.

Spanish litigation

In judgment 242/2018 issued on 19 February 2018, the Spanish Supreme Court struck down the revised provisions of I.H.T. that prevented a person resident in a country outside the E.U. and E.E.A. from accessing I.H.T. benefits under the law of an autonomous region. The decision in judgment 242/2018 in this case was followed by judgments 448/2018 of 21 March 2018 by Spanish Supreme Court and 2018/39506 of 21 March 2018 by Spanish National Court. All reached the result that persons resident outside the E.U. and the E.E.A. may access benefits granted by the I.H.T. of an autonomous region.

In judgment 242/2018, a resident of Canada inherited real property located in the autonomous region of Catalonia. She filed the I.H.T. selfassessment under Spanish national law. As a result, the I.H.T. liability amounted to €308,547.34. Had she been able to file the self-assessment under the rules of the autonomous region of Catalonia, the tax would have been limited to €189,525.91. She timely filed a claim for refund in the amount of €119,021.43 , the difference between the tax due under Spanish national law and the tax due under the regional rules in Catalonia. The tax for the Canadian resident was almost 60% greater than the tax for a resident of the Catalonian autonomous region. In a first stage hearing, the Spanish Council of Ministers denied her petition on the grounds that she was not a tax resident of the E.U. or the E.E.A. The Spanish Council of Ministers chose to apply a literal reading of the E.C.J. decision dated 3 September 2014. Consequently, it held that the E.C.J. decision was not applicable to a Canadian resident inheriting Spanish real property.

The matter was appealed to the Spanish Supreme Court, where the issue was squarely presented by the parties. Acknowledging that unequal tax treatment existed for the Canadian heir, at issue was whether the unequal treatment violated E.U. law.

The Spanish tax authorities argued that unequal tax treatment at the level of the autonomous regions was justified. They contended that discrimination did not exist because the matter did not involve unequal treatment between a resident of Spain and a resident of another Member State of the E.U. No E.U. resident suffered because the I.H.T. benefit granted by Catalonia was not extended to a resident of Canada.

Following the lead of the E.C.J., the Supreme Court held that the unequal treatment violated the freedom of movement of capital. The decision of the Council of Ministers was reversed. In the view of the court, the principal set out by the E.C.J. in Welte was squarely on point. A tax allowance granted on the basis of the residence of the decedent and the heir impairs the value of the inheritance. Such impairment violates the right to free movement of capital which is protected by Article 56(1) E.C. Spanish I.H.T. rules and related autonomous region I.H.T. rules include reductions of the taxable base. These provisions must be applicable also to persons who are not E.U. tax residents.

PATH FORWARD

Legislative action is expected. However, at this stage, it is still unclear how Spain will implement these rulings to bring the I.H.T. regime in line with the E.C.J. ruling and the E.U. principle of free movement of capital. Until legislation is enacted, heirs who are resident in a country that is not a Member State of the E.U. or E.E.A. may wish to avoid penalties by filing an I.H.T. return based on Spanish national law without claiming benefits under regional I.H.T. rules and then file a claim for refund of tax.

For I.H.T. taxpayers that are not residents of the E.U., consideration should be given to filing claims for refunds within the four-year period of limitations, which begins to run as of the final date for filing the I.H.T. return. For inheritance tax purposes, the last day for timely filing is six months after the date of death. For gift purposes, the last day for timely filing is 30 days following the taxable event.

After the effective date of Brexit, U.K. residents will no longer be granted immediate access to the I.H.T. rules of the autonomous regions but should be entitled to claim the benefits in by filing a refund. Once the Spanish law is changed to allow persons outside the E.U. to claim the benefit of regional law, British residents should be entitled automatically to lower I.H.T.

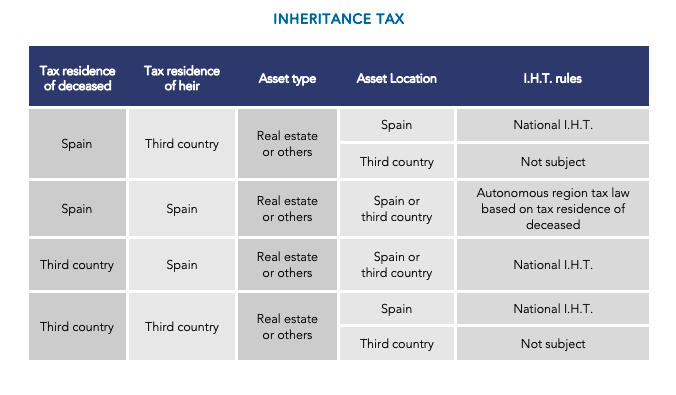

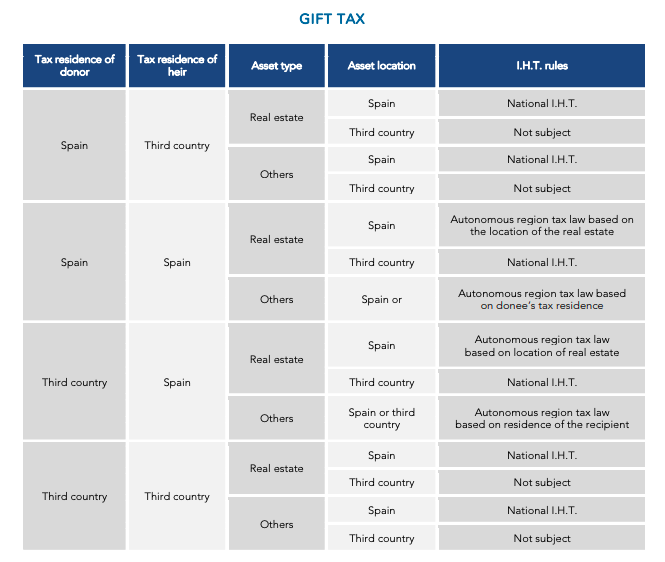

TABLE OF POTENTIAL DISCRIMINATION

Potential scenarios involving non-E.U. tax residents or elements are included, in which the potential discriminations may take place. For clarification purposes, one table deals with the inheritance tax and the other includes gift tax scenarios. In both tables, the compulsory application of Spanish national I.H.T. legislation, as opposed to tax rules in the autonomous regions, is highlighted.

No Comments